Introduction

The earlier units covered five major areas within the general

subject of management of school funds. These included the identification

of sources of school funds, concepts and skills in budgeting

for school income and expenditure, the mobilisation of financial

resources, the management and control of school expenditure

and proper school book keeping.

In this unit, we will analyse the objectives and types of

school accounts auditing and discuss the stages in the process

involved.

Individual study time: 7 hours

Learning outcomes

By the end of this unit you should be able to:

• explain the reasons and purposes for auditing accounts

• describe your expectations of the school accounts auditor

• list the types of school auditing, the records and

books of accounts used for audit purposes

• respond to audit queries

• read an audit report

Reasons and purposes of auditing school accounts

Auditing school accounts is the final stage in the process

of managing school funds. At the end of each financial year

or budget period the school head has a statutory responsibility

to prepare and present to the school governing bodies an audited

financial report.

This should give a true and fair view of the financial position

of the school.

Activity 6.1

Look up the following and study them carefully

(1) Sections in the government regulations outlining the functions

of school governing bodies with regard to financial accountability.

(2) Relevant financial regulations, principles and practices

of the Department or Ministry of Education.

Comments

In many countries, financial accountability is one of the

major responsibilities of the school board of governors/directors

and the school head. Government statutes usually include sections

outlining the financial principles and practices which boards

and heads must follow to achieve accountability for the funds

they collect and receive to run their schools.

The Ministry of Education also issues financial regulations

from time to time whereby audited accounts of a given financial

period must be submitted to facilitate financial decisions

on, for example, allocation of grants, giving loans.

The main objective of auditing is to enable the auditor to

form an opinion on the accuracy of the financial statements

prepared by the school for a given period. Auditing also helps

the head improve the school's accounting system. The secondary

objective of auditing is to detect or prevent errors. Auditing

therefore enhances the head's skills in financial management

and evaluates his or her performance.

Activity 6.2

Revise Units 3 - 5 and write simple definitions of the following

common terms in accounting:

Accounts

Account Books

Bank Reconciliation

Balance Sheet

Budget

Cash Book

Cheque

Invoice |

Journal

Financial Statement

Receipt Book

Store Ledger

Voucher

Ledger

Vote Book |

Comments

Auditing is a process whereby all accounts of the school are

examined and evaluated in detail by a competent auditor in

order to determine and report on the financial standing of

the school for the period under review. A school audit of

financial statements also establishes the credibility of the

accounting records as specified in the statutory accounting

principles and practices. To understand the audit process

you should know the common books in accounts which are the

key records used in auditing.

Activity 6.3

(1) Why does the head have to submit an audited account of school

funds to the school governing bodies at the end of each financial

year?

(2) Give reasons why auditing of school accounts is necessary.

(3) Make a list of the accounts books and records you would

consider relevant for audit purposes.

Comments

The auditor officially examines and verifies the books of

accounts and writes a final report which gives a true and

fair view of the financial status of the school. Once the

books of accounts have been examined and verified, the findings

reflect the fact that the financial transactions were made

and recorded according to accepted principles and practices.

Qualified auditors are the only ones authorised to examine

and verify the books of accounts of any formal organisation.

They are skilled in the techniques of auditing and they are

governed by international professional ethics.

Expectations of the school accounts auditor

A school head has a statutory responsibility to prepare

and submit financial statements which give a true and fair

view of the financial standing of the school. As you have

already learnt, that can only be achieved through auditing

the school accounts.

In this section you will learn about:

• the professional and personal qualifications of an

auditor

• the process involved in engaging a school accounts

auditor

• the relationship between an auditor and the school

• the information required for audit purposes.

Activity 6.4

(1) What do you understand by the phrase 'a true and fair view'

of the financial standing of the school?

(2) Who would be most qualified to give that opinion about your

school finances?

Comments

Auditing of school accounts must be done with reasonable care

and skill. The auditor must be professionally trained and

qualified with an independent mental attitude about the school.

He or she must have reputable and known personal qualities

which would support his/her opinion about the school financial

statements.

School boards of governors are corporate bodies and by statute

they are responsible for engaging auditors through the terms

of a formal contract which is binding to both parties. The

contract with the auditor must state clearly the tasks expected,the

terms of payment and date when the report must be completed

and submitted to the board. The auditor should not have any

vested interest in the school and the contract should be between

him/her and the board, but not with the school head.

After signing the contract the school head must submit to

the auditor all accounts, records and books to facilitate

his/her work. In addition, you should include all relevant

evidence to enable the auditor to draw conclusions on the

state of the school accounts. You should also be ready to

give oral evidence and to allow any inspection of assets which

the auditor may consider necessary. A thorough knowledge of

the school's financial environment, for example, regulations,

principles and practices, mechanisms of control and the school

budget, on the part of the head will greatly enhance the work

of the auditor. Auditors are in a highly privileged position

and have statutory rights to demand such information and explanations

as they consider necessary for the purpose of auditing.

Activity 6.5

Pay a visit to one of the auditing firms or audit section of

the Ministry of Education and find out about the routine functions

of the staff in the section or firm. Study also the general

procedures used in auditing small company's accounts. This will

give you some general knowledge on the subject of auditing.

Types of auditing

There are two types of auditing.

Internal auditing

Internal auditing is usually a management activity and is

a service intended to ensure regular and frequent checking

on a school's financial transactions and records. An internal

auditor is normally an employee of the school, for example

a deputy head, whose main role is to supervise the accounts

staff to ensure efficiency in the day to day management of

the school finances. It also serves to check whether all financial

transactions have taken place according to budget, to set

procedures, and following management policies. The objectives

of internal auditing may differ from school to school, but

the general aim is to promote efficiency in the school's financial

control and management.

Some schools are small entities where internal auditing may

not be necessary, especially where the accounts staff is competent.

In any case, the school head is directly involved in authorising

and approving expenses and signing cheques, and the finance

committee of the board may inspect and carry out internal

control of the funds.

External auditing

This gives an independent report on the financial performance

of the school in accordance with the terms of the contract

agreed with the school. The focus of external auditing is

on establishing the truth and fairness of the accounts. It

gives added credibility to unaudited financial statements

and records of the school's financial transactions and confirms

their compliance to the statutes.

Activity 6.6

Considering the nature of your school financial transactions:

(1) Draw up a schedule for internal auditing of your school

accounts.

(2) State three reasons why you would engage/employ an internal

auditor.

(3) Describe the difference between internal auditing and external

auditing.

Comments

It has been noted already that internal auditing is to ensure

regular and frequent checking of the financial transactions

of the school. A schedule for internal auditing should indicate

and outline the objectives, the procedures to be followed,

the frequency and the methods of communicating or reporting

the information to management.

An internal audit report should point out areas of weakness

and strength in the accounts records and books and draw the

attention of management to any irregularities in the transactions.

Information from internal auditing must be reliable, complete

and available on call to enable the head and the board to

make quick decisions where necessary.

The functions of internal auditing and external auditing

may seem to overlap but it should be noted that the former

is a management measure to ensure daily efficiency in managing

school funds, while the latter evaluates the adherence to

the accepted principles, practices and statutory provisions

of management in financial transactions. However, internal

auditing if properly done will cut down on the cost of external

auditing and greatly enhance the process.

Records and books of accounts for external auditing

Activity 6.7

(1) Make a list of the records and books of accounts you keep

in your school

(2) Consider any other information that may be relevant in the

auditing process of the school accounts and state why that information

is relevant.

Comments

Governing bodies of schools depend on financial statements

as a basis for financial decision-making. Accounts and records

are therefore very significant to the auditor who reviews

the school's systems of accounting to give his/her professional

opinion about the state of the accounts of the school.

Although many auditing procedures are designed to test accuracy

in accounting and to reveal manipulations which would conceal

the true financial situation, the main aim in applying such

procedures is to prove that the accounts are acceptable and

to give a true and fair view of the school's financial standing,

not to find faults.

The auditor's report is reached by a process of examining

and evaluating all documents or evidence pertaining to the

financial transactions of the school. In a school, books of

accounts are usually written and kept by the bursar.

A primary record in the school's financial statements is

the General Ledger. This consists of figures and records from

various journals which give the daily records of the financial

transactions in the school.

A Cash Book, where the daily cash income and expenditure

is recorded, forms one of the primary sources of evidence

that the auditor examines in the process of auditing. It states

the date, the cash received or spent, a full description of

what is bought and the actual cost of the items bought, details

of the payment voucher and number of the cheque. A petty cash

voucher may also be used along with the Cash Book. Almost

all assets, liabilities, income and expenses clear through

the cash account, and the auditors will spend time carefully

examining the Cash Book to establish the validity and reliability

of other financial statements.

Payment vouchers, purchase invoices, receipts books, books

of inventories and cheque books are primary documents which

must be submitted to the auditor for verification, inspection

and evaluation before a report is written and an opinion is

given on the school's accounts.

Bank reconciliations and bank statements which compare the

balance in the bank with that shown in the school's records

can reveal book keeping errors either by the bank or by the

school clerk as well as unauthorised withdrawals. These should

be submitted along with other documents for auditing.

Activity 6.8

(1) Study a sample of a Cash Book and list all the information

that is found or recorded in it.

(2) Give reasons for keeping a petty cash voucher in your school.

(3) Read the case study below and make entries in the appropriate

school accounts books recording the financial transactions described

therein. Trace the steps to be taken to record all the transactions.

Case study

Mr Okello, head of the Science Department in Shimoni Demonstration

School, submitted a requisition to buy chemicals for the end

of term examinations. Mr Okello has contacted the suppliers

and he has obtained a supplier's invoice No. 0658 indicating

the quantity of the items: 10 tins of sulphur costing shs

5,000/- each and 10 tins of potassium costing shs 76,000/-

each. The invoice has been submitted to the school accounts

clerk who has checked vote No. 031 on scholastic materials

and has confirmed that there is a balance of shs.978,000/-

which is sufficient to cover the cost of the chemicals.

The suppliers have delivered the chemicals in the quantities

indicated on the local purchase order No. 112. The materials

are accompanied with a supplier's invoice dated 29th February

1992, indicating the details of the materials and the cost

of each item.

Mr Mukasa the storekeeper and Mr Okello have checked and

found the materials in order as per the local purchase order

and the supplier's invoice. The chemicals bought have been

recorded in the Store Ledger on folio No. S/10/92.

All invoices have been received and recorded by the accounts

clerk in the Journal or Ledger. You have also authorised payment

for the chemicals and payment instructions have been given to

the accounts clerk. A payment voucher No. 5465 dated 3rd March

1992 has been made out and you have endorsed it. The voucher

gives quantities of what has been bought in and gives the total

cost as shs 126,000/- (one hundred twenty six thousand shillings)

only. A cheque No. 02568 for that amount has been written on

6th March 1992, payable to ACPY, the suppliers. A cash receipt

No. 136 dated 25th March 1992 has been issued by the suppliers

on 29th March, 1992.

Comments

You have already learnt that a Cash Book is a very important

book of accounts because all cash income and expenditure go

through it. The auditor therefore, spends quite a lot of time

and care in examining the Cash Book. Wrong or inadequate entries,

plus omissions made in a Cash Book, will greatly affect the

auditor's opinion on the state of the school books.

You should also note that before any entries are made in

the Cash Book all other documentary evidence of the transactions

like vouchers, invoices, receipts must be checked and certified

to ensure that all procedures and regulations were followed

and no errors were made.

A thorough knowledge of how a Cash Book is written will enhance

your internal financial control and it will enable you to

understand and appreciate the purpose of auditing school accounts.

Reading an audit report

Activity 6.9

Look at your school's recent audit report:

(1) List the main features in its format (schedule).

(2) Analyse its contents briefly.

(3) Point out its weaknesses if any.

Comments

An audit report should be clear, constructive and concise.

The auditor will point out in writing to the authorities:

• any weaknesses/strengths in the accounting system of

the school

• deficiencies in the financial control system

• inadequacies in the financial policies and practices

• non-compliance with accounting standards and legislation.

The report also explains any implications of the above points

and gives advice or recommendations for improvement. The auditor

should give in clear terms his/her professional opinion on

the state of the accounts.

One of the main schedules in an audited report is the Balance

Sheet. This is a summary statement of all assets and liabilities

of the school by the date of the report in reference. However,

an audit report should also have the following components:

• a title, that is, Auditors Report

• a statement as to whom addressed, for example, The

School Directors

• a description of the scope of the audit, showing the

books examined and the tasks executed by the auditor according

to the contract and audit standards

• the auditor's opinion on the state of the school accounts

• the auditor's address

• the date of the report.

The auditor's opinion can be unqualified, qualified or adverse

depending on the state of the books of accounts and any other

evidence the auditor may have examined and evaluated. An unqualified

opinion is positive and satisfactory and a qualified opinion

indicates that the auditor has some reservations about the

state of the school's accounts.

Responding to audit queries

Activity 6.10

You may have already been involved in the auditing of your school

accounts. Consider what queries the auditors may have raised

about your books of accounts and about any other submissions

you made.

Comments

You have already learnt that the primary objective of an audit

is to enable the auditor to determine the accuracy of the

school's financial accounts. You have also learnt that the

auditor gives his opinion on whether or not the accounts give

a true and fair view of the financial standing of the school.

A secondary objective of the audit is to detect errors in

the accounts and advise the board on how to improve the book

keeping standards.

Audit queries can be raised where errors have been made in

the records. These can be due to a wrong entry or an omission

of some vital information. When an error is located by the

auditor he raises a query to the head seeking for an explanation.

For example, he may raise a query where the Trial Balance

does not agree with the statements of accounts.

In response the head can take any of the following steps:

1 Submit further information to the auditor on the queried

items.

2 Let the auditor inspect the assets and stores.

3 Go over the Trial Balance with the auditor checking:

• the totals

• lists of debtors and creditors

• transfer or entry of all the accounts books to the

Trial Balance

• all figures in the Trial Balance.

4 Go over the cash book and over all other financial documents

and statements to locate errors, omissions or any evidence

of fraudulent payments that may have been made in the transactions.

5 Consider making adjustments by reviewing assets against

liabilities.

6 Consider writing off bad debts.

A Trial Balance summarises the effect of all financial transactions

on the school accounts and it helps you and the auditor to

get a preliminary view of the accounts before a Balance Sheet

is written and an audit report is finalised.

Where you, as the school's financial manager, fail to answer

all the queries satisfactorily the auditor will present what

is termed as a qualified audit report. This is a report where

the auditor has been unable to obtain all the information

and explanation he or she considers necessary for the audit.

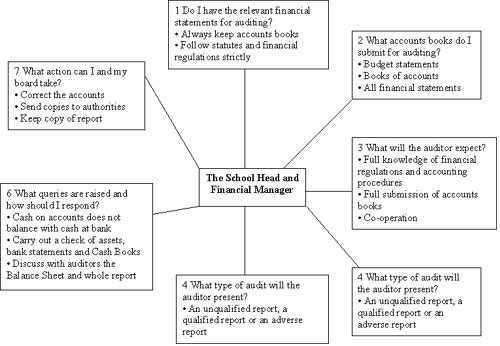

Summary

The diagram below gives you a brief summary of the various

stages involved in the auditing of school financial statements.

These correspond generally with the topics which you have

covered in this unit. The summary diagram is also based on

questions which you may pose to yourself to make a checklist

of what you have learnt from the unit.

Fig 10 Summary diagram

|