Introduction

The effectiveness and efficiency of the education system

largely depends on the quantity and quality of the instructional

materials available. Because the purchase of instructional materials

requires large sums of money it is vital that school heads know

how to manage school funds.

Individual study time: 7 hours

Learning outcomes

By the end of this unit you should be able to:

• define expenditure

• define finance

• identify the procedure of expending school funds

• explain accounting procedures in the management of

school funds

• display some knowledge of management and controlling

of school funds

• practise proper accountability procedures for school

funds.

Financial resources and management in schools

This unit does not comment on the various sources of school

funds nor on the need for proper budgeting in schools. These

have already been discussed in Units 1 and 2. The present

unit will therefore deal with:

• the procedure for expending school funds

• the processes of controlling school expenditure

• accountability of school funds.

Before we do so, remind yourself of what was covered in Units

1 and 2 by doing the following:

Activity 5.1

(1) Briefly explain budgeting.

(2) What is income and what is expenditure?

(3) Differentiate between line-term and programme budgets.

(4) What is finance?

(5) Explain financial management.

Comments

The following are useful additions to the answers you may

have given:

1 Budgeting is a process of preparing estimates or the statement

of expected income and proposed expenditure.

2 Income refers to how the amount to be used will be raised

and how much it is.

3 Expenditure is the amount that was/will be allocated to

be spent on various functions.

4 Programme budgets are benefit oriented, based on set goals,

while line-term budgets are cost-oriented.

5 Finance refers to money and other resources which assist

the school in achieving its objectives.

6 Financial management covers the administration of financial

resources including money and how to generate it.

The proper management of school funds is an important component

of good school administration. Funds constitute the nerve

centre of the school. They must therefore be properly managed

for the school to achieve its objectives.

Procedure for expending school funds

This is referred to as the implementation stage of the

budget or budget administration. In practice this is the execution

of planned school programmes with proper expenditure of funds

as shown in the approved budget. The budget becomes a very

important document for managing the finances of the school.

Before beginning to implement it, you need to explore its

structure so that you understand its basic requirements, as

well as the opportunities and threats it may present.

Activity 5.2

(1) Reflecting on your experience as a school head, find out

the following:

- the procedure for expending school funds in your country;

- current financial regulations on the management of school

funds;

- the authority which issues the regulations.

(2) Study your findings and indicate how they assist you in

performing your function or whether they create problems.

Comments

In addition to what you have found out the procedures for

expending school funds are usually as follows:

Regulations

The Ministry of Education issues specific instructions with

regard to the spending of and accounting for funds. For example:

1 Funds released by the MoE for one purpose should not be

diverted for another purpose (see note below).

2 It gives guidance on how much you can spend within the usual

procedure on a particular item.

3 It compels you to obtain approved authority for spending

on an item.

4 All expenditures incurred should be recorded in an acceptable

manner according to the Standard Accounting Practice (SAP).

If the need for expenditure arises,contrary to the approved

budget, written authority should be sought from the MoE or

the governing body or PTA. Discuss with your colleagues the

implications of the regulations in your country related to

this issue. What problems have arisen recently?

Procurement procedures

It is advisable to use the Tender Board or Purchasing Body

to control expenditure. If there is any bidding, it is done

by the board of governors through its Finance Committee. Interested

parties are not allowed to supply goods/services to the institution.

It is not always easy to protect yourself from this last problem.

Proforma invoice

A proforma invoice is issued when payment is made before goods

are delivered. When one cannot be obtained an officer responsible

for implementing a task raises a claim in respect of the task

and submits it to you for approval. Then the funds so approved

can be released.

Order forms or delivery notes

The purchase of goods, furniture or maintenance works should

be done by order forms or delivery notes. You must ensure

that goods and services ordered are delivered before signing

the delivery notes.

A cheque

This is made to ensure that the order to pay is legal. You

should check if the payment claimed was effected; that goods/services

paid for were delivered; and that the transaction was properly

recorded. It is improper for you to ask the chairman of the

board of governors/PTA executive committee to sign a blank

cheque or for a cheque to bear only the signatures of yourself

and the bursar.

Financial flexibility

If flexibility is possible, the total amount of money available

to the school can be enlarged and better value gained. It

can be done in two ways:

Borrowing of funds from one vote to another: Internal borrowing

is justifiable because under-spent accounts can compensate

for overspent accounts. For example, maintenance of vehicles

( a very expensive item) may lead to borrowing from general

accounts. Internal borrowing also helps to counteract uncontrolled

prices and inflation. However, such adjustment must be done

with the approval of the governing body.

Carrying balances forward: An increasing number of institutions

carry forward unspent capitation from one year to another;

and over-spending is carried forward as a deficit to be paid

off next year. There are three advantages of this practice:

1 Institutions can plan their expenditure if necessary outside

the limits of one financial year.

2 There is no risk of losing unspent funds.

3 Schools spend less time on administration of funds, because

there is no longer any need to balance expenditure exactly

against income.

Activity 5.3

Recollect what you have read and thought about in this section

of the unit and write answers to the following:

(1) Name the items on which a school spends money.

(2) Give reasons why there is a need for you to be flexible

in financial management.

(3) Name two ways of effecting financial flexibility.

(4) Explain 'capital' and 'recurrent' expenditure.

(5) Group the items you buy for your school into the above categories.

Accountability of school finance

Definitions

Accounting: This involves checking to ensure that the

order to pay is legal, that payment is effected and recorded

in the general financial account covering all money spent

in accordance with the budget.

Financial information: This is not useful unless it

is expressed in monetary terms like internationally acceptable

currencies, such as dollars, pounds sterling, yen, etc. or

local currencies, such as the naira, cedi or shilling.

Accountability: This refers to budget control. It

is the evaluation and guidance of budget administration activities

throughout the school's fiscal year.

Budget control: This acts as a device for assuming

accountability to prevent misappropriation, embezzlement and

illegal spending of funds. It deals with monetary records,

which keep account of how money is spent, and therefore helps

planning for the future.

Activity 5.4

In view of the definitions of terms given above:

(1) Name some of the finance records you use when accounting

for school funds.

(2) Give reasons to justify the use of such records.

(3) Describe the accounting principles involved while making

financial records.

Comments

Make sure you have included the following in your points:

The importance of financial records

Financial records are records of day-to-day financial operations

in a normal situation in school administration. These records

are important because:

• they are the basis for decision-making on any financial

matters

• they provide a means of tracking the growth or decline

of the school's assets or liabilities

• they form the basis for determining the value (appreciation

or depreciation) of school property

• they are guidelines to indicate the financial position

of the school.

Budgetary records

They are systematic ways of accounting for budget implementation

by keeping basic records. The following documents are essential

for a school or college for the effective handling of funds

:

Receipt Books

All payments and receipts should be presented with the proper

evidence. You should have receipt books whose leaves/pages

must be numbered to enable the detection of lost leaves or

receipts. Receipts should be issued at least in duplicate

for money received for example, fees. They must also be received

for money paid out.

The receipt is the first evidence of cash spent or received.

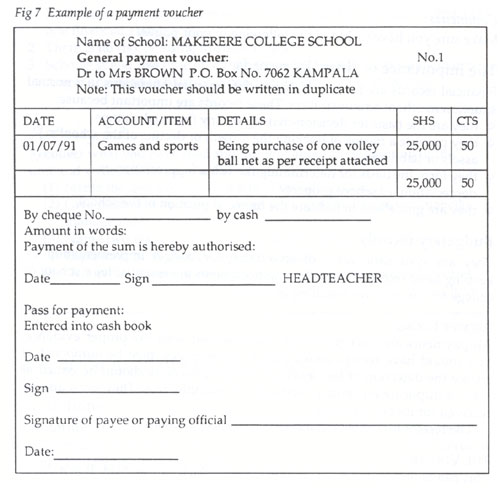

The Voucher

This can be in book form or in loose sheets which can be filed.

It is a document detailing the purpose of any payment made,

the date of the payment, the amount, the budgetary vote or

item within which the expense is being incurred and the authority

that has sanctioned the payment. An example of a payment voucher

is given in Fig 7.

Fig 7 Example of a payment voucher

Note that:

1 The voucher has to be written and signed first before money

is released.

2 It must bear a number that can be quoted.

3 Receipts obtained after purchases must be attached to the

voucher.

4 This document informs one as to how public money has been

used.

The Cash Book

This is a book into which information is entered on a daily

basis, giving details of money received, such as fees and

money paid out, such as for buying school chalk. This book

has to be balanced daily so that cash received that day must

be balanced against cash spent on the same day. That way,

you are immediately aware of the day's collections and spending.

Cheques received or paid out all form part of the day's income

and expenditure respectively.

A Log Book or Journal

As financial controller you should open a log book in which

all financial transactions are recorded each day. This book

can be referred to as a journal that is a record of financial

transactions done on a daily basis.

Financial Ledgers

For records of account to be meaningful, information from

the journal should be posted in ledgers. These account books

record the gains and money spent by the school on particular

days. The record emphasises the items in the income and expenditure

sides and the net balance for that date.

The following are the types of ledgers operated in schools

and colleges:

The General Ledger: This is a book that contains all

major items of the budget, for example, food, lighting, stationery.

A few pages are allocated to each budget item and on these

pages are recorded the daily expenses made under the particular

item. An example is given in Fig 8.

Note that all information in receipt books, vouchers and

cash books have ended up in the ledger. It offers a clear

picture as to which items are frequently purchased.

The Fees Ledger: This ledger records all information

on each student's fees payment that is date, amount, total paid

to date and balance outstanding, or carried forward. At a glance

it is easy to assess the extent of fee collection, to obtain

a list of fees defaulters and to know accurately how much fee

money is still outstanding. The information has to be recorded

as soon as the fees are paid in order to avoid problems caused

by the loss or misplacement of receipts and receipt books or

accumulation of work.

Fig 8 Example of a General Ledger

| Date |

Voucher No. |

Food |

Expenses |

| |

|

|

shs |

cts |

| 08/5/91 |

192/8 |

Beans |

750,000 |

00 |

| 12/5/91 |

192/8 |

Cooking oil |

100,000 |

00 |

| 07/6/92 |

193/50 |

Sugar |

850,000 |

00 |

Credit Ledger/Black Book: This is a book that contains

the list of the school's debtors, the amount owed to the school

by each, dates when settlement was made and the outstanding

amount still to be paid. It is necessary to keep checking

this book to ensure that your school has recovered what is

due to it. You ensure this by keeping the entries in the book

up-to-date.

Vote Book: This is a book which essentially shows

how much is left of the vote for an item. It records the total

amount voted for the item as per the budget, the daily purchases

made under that item and the balance left after these purchases.

It makes it easy for you to see whether you are over-spending

or not and is a particularly useful check on high spending.

It is therefore advisable that you maintain a Vote Book. You

will find an example in Fig 9.

Fig 9 Example of a Vote Book

| ITEM VEHICLE MAINTENANCE |

VOTE shs. 9,000,000 |

|

| Date |

Purchases |

Amount |

Balance |

| 07/9/91 |

4 tyres |

1,000,000 |

8,000,000 |

| 01/10/91 |

30 litres of oil |

50,000 |

7,950,000 |

| 17/11/91 |

2 new headlamps |

500,000 |

7,450,000 |

| 25/11/91 |

New windscreen |

1,000,000 |

6,450,000 |

The Green Book: This is a book that lists all those

who have been given money for purchasing, the amount given

and all the details related to it.

General Stores Inventory Book: Apart from Teachers'

Houses Inventory Book and a Book Stores Inventory Book, you

should maintain a General Stores Inventory Book where equipment

like slashers, hoes, etc. are recorded. The purpose of these

inventory books is to enable the school administration (you)

to keep track of school property and make replacements accordingly.

Activity 5.5

Using the information given above:

(1) Outline the procedures and the accounts books used in you

school for recording:

- a payment in (e.g. fees);

- a payment out.

(2) Write out a payment voucher to your food supplier. See Fig

7 for an example.

(3) Indicate how you would use a Cash Book.

Basic accounting processes

Once you know how to keep the account books properly,

you can turn your attention to thinking about how to analyse

the financial data now available. To do this, you should know

the basic accounting processes. These are:

• preparation of financial statements such as: income

statements, balance sheets, reconciliation statements and

flow of funds statements, etc.

• analysis and preparation of financial statements to

arrive at hidden facts and draw corresponding conclusions

• preparation of comprehensive financial reports

• rendering of financial advice on decisions to be made

in the light of the conclusions reached.

In practice, to be able to perform the above functions, as

the accounting officer of the school, your duty is to initiate

financial plans for your board of governors or PTA to adopt.

You are at the centre of the school's financial plan and therefore

you need to help those with whom you work to formulate proper

plans. If that is achieved, then your job of mobilising funds

becomes relatively easy. Remember, no parent will contribute

more money to the school if the plans are not well defined.

Note that knowledge of accounting will assist you in the

day to day management of the funds of the school. It is important

so that you have some insight into the financial planning

and organisation of your school's finances.

Trial Balance

We first look at the Trial Balance which is an important tool

in accounting and gives a list of all the accounts used by

the school at the appropriate value and time. Its main purpose

is to enable you to know precisely the balance in each account

at say fortnightly or weekly intervals. This enables you to

know at any point of the fiscal year which items are being

deflected first. It helps you to put a brake on if you are

spending too fast on one item.

The School Balance Sheet

This is the most important financial document for the school.

It is a financial statement of the school at a given date.

It must reveal all the assets and liabilities of the school

at a particular time, for instance, at the end of the financial

year. Before you proceed, ensure that three of the accounting

terms used in the Balance Sheet are clear.

Activity 5.6

Define the terms

- financial statements;

- assets;

- liabilities.

Comments

The importance of a school's Balance Sheet lies in the revelation

of all the assets and liabilities of the school at the date

in question. The terms 'financial statements', 'assets' and

'liabilities' should therefore be understood in the context

of the Balance Sheet to mean the following:

Financial statements: These show at a glance the amount

spent on various items. They convey the financial status (blue

or red) of the school at a particular time.

Assets: These are the properties or belongings of

the school which appear in the Balance Sheet. They may be

classified as long or short term assets, namely fixed or current

assets.

Liabilities: These are the debts or claims of outsiders

against the belongings of the school as at the date when the

Balance Sheet is drawn up. They too can be long term or short

term in nature, namely fixed or current liabilities.

You may wish to make a quarterly Balance Sheet, or an annual

one depending on the practical problems of your school. Some

heads make it monthly.

Annual accounts and Balance Sheets have to be prepared and

a copy sent to the MoE at the end of every financial year.

Balance Sheets should be the main financial concern of a

new school head.

Comments

If you look at a school balance sheet, you should be able

to see:

• the total value of fixed assets

• the total value of current assets

• the sources of funds

• the debts to which you would give immediate attention

• debts which require payment - but not in the near future

• the total value of assets possessed by the school and

how much of this is claimed by outsiders.

Note that:

1 Changes in your financial plan will cause changes in the

school Balance Sheet.

2 Such changes should be recorded systematically in the record

books already referred to.

3 The Balance Sheet requires the proper keeping of all records

of account such as receipts, vouchers, inventories, ledgers,

etc.

Activity 5.7

You can now look back at the whole of Unit 5. Recollect what

you have learnt and answer the following questions:

(1) Explain the procedures for expending school funds.

(2) Give three reasons for exercising flexibility in financial

management.

(3) Show, using specific examples, how failure in conforming

to book-keeping and accounting functions may lead to the mismanagement

of school funds.

(4) How can you employ the basic accounting concepts in maintaining

financial records in the school?

Summary

In this unit you have learnt about:

• expending and accounting for school money

• the procedure for expending school funds

• the financial regulations of your Ministry of Education

• the need to exercise flexibility in the management

of funds ù the importance of maintaining proper financial

records

• the operation of proper and regular school balance

sheets

• the need for a good financial plan. |